Why Canadians Will See a Little More in Their Paycheques

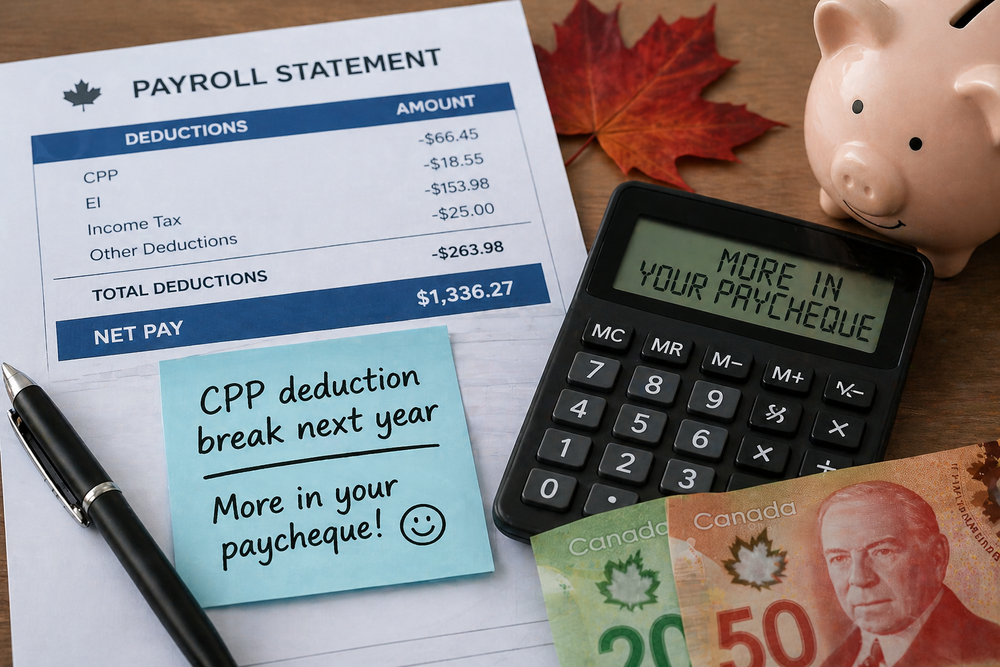

A small CPP deduction break is coming for Canadians, easing paycheque pressure and offering modest financial relief while keeping retirement benefits strong.

A small CPP deduction break is coming for Canadians, easing paycheque pressure and offering modest financial relief while keeping retirement benefits strong.